Firm Intro

Lumix Traders is a Sydney-based firm built on a single conviction - that trading is a craft, and that a craft rewards the prepared. We operate across the foreign exchange and CFD markets, and we serve two distinct constituencies. For retail participants, we partner with established brokerage firms to provide analysis and structured education to produce work aimed at building durable market capability and disciplined process rather than the pursuit of the next quick position. For wholesale clients such as small and mid-sized hedge funds, proprietary trading groups, and professional traders operating internationally, our focus is the infrastructure that determines outcomes under pressure: hedging, market execution, and workflow efficiency across global CFD and derivative markets.

The Lumix Lens is where the two constituents meet. Each edition follows the architecture of a macro overview, the environment that shapes every position; to micro, the specific instruments in which the environments become tradable; to method, the way a disciplined participant navigates the terrain (which will not be included in this week's intro). And of course, we do not issue recommendations. Our purpose is to demonstrate how we think, because in markets a repeatable process is the only durable advantage, and the present moment is an unusually instructive one in which to show our reasoning. What follows is an attempt to execute that properly.

Summary Table: Gold Macro Driver

| Driver | Indicator | Current Level | Direction(90) |

|---|---|---|---|

| Real Yields | DFII10 (10y TIPS) | 2.06% | +0.34pp |

| USD | DTWEXBGS (Broad) | 119.3 | +1.47pts |

| FED Policy Rate | Fed Funds Target | 3.50-3.75 | Flat |

| Fed Balance Sheet | WALCL | $6,704 B | +$90.6 B |

| Inflation Exp. (10y) | T10YIE | 2.39% | +0.14 pp |

| Forward Inflation | T5YIFR | 2.24% | +0.14 pp |

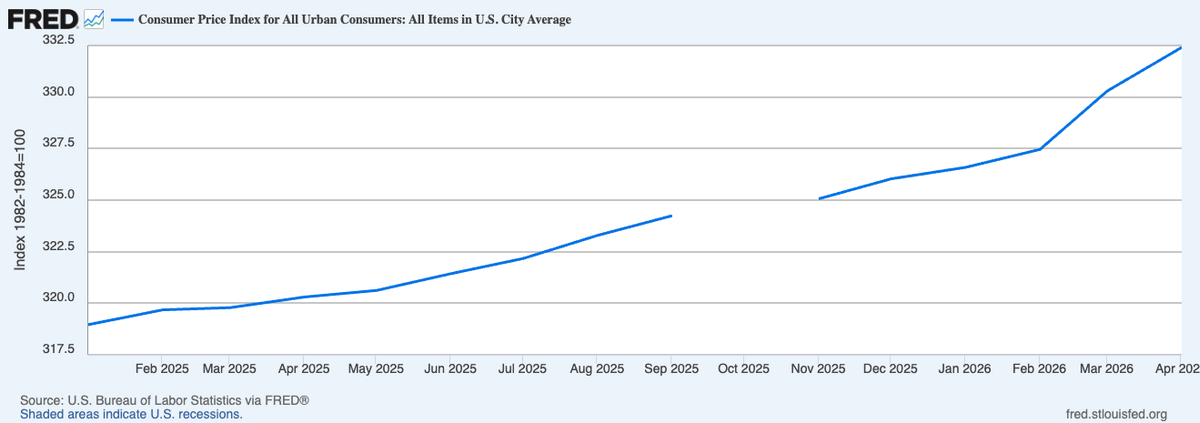

| Realised Inflation | CPI Headline (Apr) | 332.4 | Flat |

| Labour Market | Unemployment | 4.3% | Flat |

| Gold Price Action | GC=F Close | $4560.5 | -14% Since March |

News Overview

2026/05/15: Trump-Xi summit produces no concrete steps toward Middle East resolution, 10-year yield top 4.55%

2026/05/20: US and Iran trade military strikes, oil prices spike, doubts about peace deal

2026/05/27: Reports that US and Iran reached a tentative 60-day MOU to extend the ceasefire.

2026/05/28: S&P500, NASDAQ, Dow closes at record high on positive cease fire reports. Gold initially falls to a two month low on easing oil-driven inflation fears then recover.

2026/05/29: Trump says he needs "a couple days to think" about the deal. Silver opens +4.6% to truce extension news, Gold ticks up to $4560.40.

Micro Drivers

I. The Regime Change: from disinflation to a supply-driven inflation

It is worth recalling how recently the consensus pointed in the opposite direction. As of January 2026, the dominant 2026 narrative across rates and currency markets was one of orderly disinflation. US headline inflation had cooled to 2.4% which is the lowest in roughly a year. Survey-based inflation expectations were easing. If we can recall, the debate among market participants was not whether major central banks would cut rates over the coming year, but how many cuts to price.

The entire framework has been overturned in the space of three months, and the cause is not domestic demand but an external supply shock.

The April Consumer Price Index (CPI) showed headline inflation accelerating to 3.8% YoY, the fastest pace since May 2023, and a sharp escalation from 3.3% in March and 2.4% at the start of the year. The proximate driver is unambiguous with petrol and heating fuel leading the move, as energy costs rose roughly 18% over the year which is the steepest annual increase since 2022. These are the symptoms of a cost-push shock manifesting in the price levels.

The core of why this matters is reduced to the distinction between first-round and second-round effects. It is also the lens through which the rest of the analysis should be read. A first-round effect is the direct, mechanical impact of higher energy prices on the energy component of the index. When isolated, it is a one-off change in relative prices and conventional central-banking practice is to look through it. Monetary policy cannot lower the price of crude, and tightening in response to a temporary supply disruption risks compounding the damage to growth. The substantial risk lies in the second round effects. It is the process by which an initial price shock seeps into core goods and services, into wage-setting, and most consequentially into the inflation expectations that shape behaviour. As expectations begin to drift, an external shock can metastasis into self-sustaining domestic inflation.

II. The Central Bank's Dilemma

The Federal Reserve finds itself in a Game Theory-esque situation where it is confronted with a supply shock and it faces two unattractive options with low payoffs. If the Fed decides to look through the shock (accomodate) and accepts a temporary overshoot in inflation on the rationale that the cause is external, the relative-price effect is one-off, and tightening would deepen the hit to an economy already absorbing an energy tax. Or it can respond by pre-emptively tightening rates to defend the credibility of its inflation target and to prevent expectations from de-anchoring, at the cost of amplifying the downturn. Neither strategy yields a Pareto-Optimal outcome - the first action risks inflation and the second risks growth. There is no option that avoids both, closely resembling a Prisoner's Dilemma. The Nash outcome leaves one objective unfulfilled, and there is no simple escape to simultaneously achieve both goals. What the Fed can do is use credibility and communication as tools to shift expectations (effectively treating the private sector as another player) and thereby improve the game's outcome. But ultimately the dilemmatic nature of this supply shock game means one mandate will suffer no matter what.

However the Fed's dilemma can be seen as dynamic. Models show the optimal policy can be a trigger or threshold strategy in a repeated-game sense: tolerate isolated supply shocks up to a point, then pivot sharply if inflation threatens to become persistent. In effect, the Fed's policy is like a mixed/trigger strategy: initially "cooperating" by accommodating, then "punishing" by aggressively tightening once a credibility threshold is breached. However, Fed officials note this depends critically on expectations. Strong monetary credibility means inflation expectations stay anchored and allow some accommodation. But if credibility falters, the Fed must act pre-emptively: as Governor Ferguson emphasized, "monetary credibility helps the central bank do its job" by anchoring expectations, and central bankers must "reinforce credibility" by leaning against inflation before it builds.

The internal disagreement within the institution is the most honest reflection of that dilemma. The Fed held policy rates 3.5-3.75% since December, but the late April meeting produced four dissents, and the minutes released in May solidified the fracture. A majority of officials now judge that further rate increases could become necessary if the conflict continues to feed inflation. The dissents themselves capture the spectrum of the debate, ranging from a preference for cutting with the logic that policy should support an economy being squeezed by an external shock, to objections against signalling any easing bias at all while inflation is accelerating. An economy that began the year debating the pace of cuts is now contemplating hikes, and the committee cannot agree on the direction of the next move.

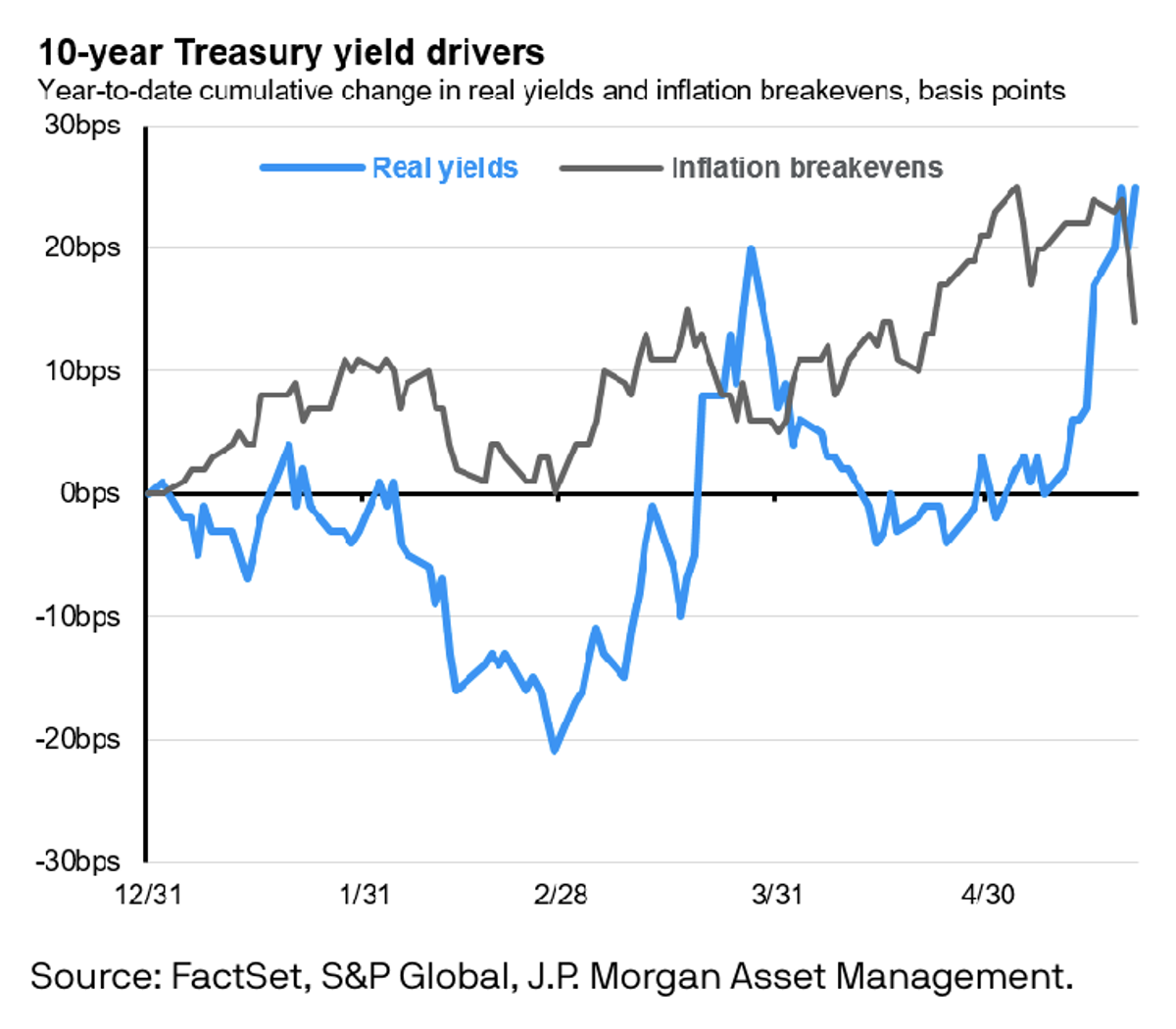

From our observations, markets have drawn their own conclusions. The probability of rate cuts have been priced almost entirely out of their curve. The US 10-year Treasury yield has climbed back towards 4.46%, near its high for the year, while the two-year yield sits around 4.0%, above the current funds rate, an unusual configuration that embeds expectations of further tightening rather than easing. With nominal yields elevated and inflation expectations rising in tandem, real yields have remained firm, a fact that becomes important when we turn to gold. Layered over all is a transition in leadership from Jerome Powell to Kevin Warsh, who was tapped by Trump in hopes of a rate cut, adding a further dimension of institutional uncertainty to an already complex policy juncture. The next decision on 16-17 of June will arrive alongside updated economic projections, which will be the first formal read on how the committee intends to resolve the tension it has so far described.

III. Geopolitical Core: The Iranian War and the Strait of Hormuz

Since Trump and Israel launched surprise airstrikes on Iranian military and government targets on February 28th, the Islamic Revolutionary Guard Corps (IRGC) formally confirmed the closure of the Strait of Hormuz on March 2nd, 2026. The Strait of Hormuz carried in the order of 20 million barrels per day before the conflict - roughly a fifth of global oil supply, and the International Energy Agency describes it as the world's most important oil artery. The defining feature of Hormuz is that it has no adequate bypass. The alternative pipeline routes can absorb only a fraction of the volume that normally transits the waterway. When flows through it are interrupted, the consequences are immediate and global because most of the world's seaborne crude and a large share of its liquefied natural gas depend on a single, narrow passage.

Since the conflict escalated at the end of February, the scale of the disruption is difficult to overstate. By the IEA's accounting, this is the largest supply disruption in the history of the oil market. OPEC production has fallen by more than 30% on the order of 9.7 million barrels per day, with output collapsing in March and remaining severely curtailed since. Global oil supply plunged by roughly 10 million barrels per day in March alone, and cumulative production losses from Gulf producers have run past a billion barrels. The exporters most affected such as Saudi Arabia, Iraq, Kuwait, and the UAE are precisely those that were the only members of the group with the ability to raise output.

The price action followed. From a pre-conflict range around US$60–70, Brent climbed more than 50% within weeks and pushed above US$120 which reached a four year high at the peak, with some forecasters warning that a prolonged closure of the strait could drive prices toward US$150. In recent sessions, Brent has retraced toward the mid-US$90s, pulled lower by hopes that Washington and Tehran can reach an agreement to de-escalate and reopen the waterway. But that relief has been violent and two-sided as prices have repeatedly snapped higher on reports of fresh strikes and faded on diplomatic signals, frequently within a single trading session.

Crude Oil

Oil is where the macro narrative becomes a tradeable contract, and it is a near-perfect case study in why market structure matters more than point forecasts. The most useful real-time gauge of the tension described above is not the spot price but the shape of the futures curve. A market in steep backwardation where prompt contracts trade at a premium to those further out, signalling acute near-term scarcity which is a willingness to pay up for barrels today. That structural signal can persist even on days when the spot price is falling on a diplomatic headline, which is exactly why anchoring to a single number on a screen is so misleading in this environment.

From Lumix's data we are seeing WTI large speculator net positions stood at 192,302 contracts as of late April, down 14,239 contracts from 206,541 the prior week signalling a meaningful reduction that places the three-year strength score at 49.2%, precisely at the midpoint of the historical range. That figure is worth pausing on. It reflects neither the crowded long that would signal a market stretched by momentum chasers, nor the capitulation that historically marks a durable floor. Commercial hedgers, whose positioning typically reflects near-term supply and demand fundamentals, sit at a similarly non-committal 47.5%. What this configuration tells us is that the market's largest and most informed participants are not committed to a direction, which is precisely the condition one would expect when the dominant variable is a geopolitical negotiation whose outcome cannot be modelled. The one exception is the small trader cohort, bullish at 68.9%, but retail conviction at the extreme of a volatile move has historically served as a caution rather than a signal to follow. In aggregate, positioning does not support the thesis that crude has been bought by momentum in a way that leaves it technically fragile.

Gold

Gold trades near record highs around US$4,500 an ounce, having crossed US$4,000 only last October. The conventional cyclical drivers are all present: safe-haven demand as geopolitical risk has risen, gold's traditional role as an inflation hedge, and shifting expectations for the dollar. However there is a tension that is overlooked. Gold pays no yield. In textbook terms, the firm real yields and resilient dollar described above should be a powerful headwind for it, raising the opportunity cost of holding a non-income-producing asset. So technically by the old playbook, gold should be under pressure. It is instead trading near all-time highs.

The resolution to that phenomenon, is in our view the most important structural development in the precious-metals market, and it lies in the identity of the marginal buyer. For most of the modern era, gold's price at the margin was set by Western investors: ETF flows and speculative positioning that are acutely sensitive to real interest rates. That marginal buyer has changed. According to the World Gold Council, central banks purchased roughly 863 tonnes of gold in 2025, the sixteenth consecutive year of net official-sector buying and more than double the pre-2022 annual pace, with the Council projecting a still-exceptional 750–850 tonnes in 2026. We believe it is a strategic reserve diversification, which poses as a deliberate reallocation away from dollar-denominated assets toward a politically neutral store of value, driven by sanctions risk and geopolitical fragmentation and visible in the decline of the dollar's share of global allocated reserves to roughly 57%.

A buyer motivated by sovereign strategy rather than return is structurally price-insensitive as it establishes a demand floor that does not yield to higher prices or higher rates the way speculative demand does. This is why the historical relationship between gold and real yields has temporarily diverged. We believe that reading the signal from a top-down perspective, rather than mechanically applying a rule that no longer governs the marginal trade is important for the current landscape.

Conclusion: Going Forward with Lumix

The macro environment entering June is one defined by competing forces. The disinflation consensus that opened the year with headline CPI sat at 2.4% and debate over rate cut has been dismantled in three months by a supply shock of historic proportions. April CPI printing at 3.8% YoY, driven by an 18% annual surge in energy costs, has forced a Fed holding at 3.50-3.75% to contemplate hikes rather than cuts, with four dissents at the April meeting capturing the depth of the internal fracture. The 10-year yield climbed back toward 4.46% and real yield firmed at 2.06% representing the market drawing their own conclusion ahead of the June 16-17 decision.

With the June 16-17 Fed decision and the fate of the Iran ceasefire MOU all due to land within days of each other, the next week may well be the most consequential of the year for this trade.

This is where we want to set expectations for what follows. Lumix is establishing itself as a weekly publication, with the commodity market positioned at the centre of our coverage. As the current energy-driven inflation shock demonstrates, commodities can no longer be treated as a satellite allocation. They now represent the clearest available read on the cycle, and we intend to track them on a consistent weekly basis.

Each update will serve two functions. The first is to provide a structured assessment of the events the broader market is monitoring and the principal geopolitical flashpoints, accompanied by a clear view of what is already priced in and where the residual risk sits. The second is the Lumix Radar, our coverage of the stories we believe are being overlooked or mispriced. These are the second-order developments that rarely reach the headlines but frequently come to define the quarter that follows.

Underpinning this coverage is our in-house quantitative model, which we are committed to refining with each cycle. The objective is not a static framework but one that compounds over time, tightening signal quality, stress-testing our positioning against each new data print, and feeding more rigorous, evidence-based conviction into the calls we present. The weekly cadence is what makes this possible. Every Fed meeting, every CPI release, and every material move in energy markets becomes a further data point that sharpens how the model interprets the next.

We therefore encourage you not to miss our next weekly update. For everything you need to stay informed, visit us at lumixtraders.com.au.

Disclaimer: The content published by Lumix Traders Pty Ltd (ABN 35 678 305 738) is intended for educational and informational purposes only. It discusses general market activity, macroeconomic conditions, industry trends, and related commentary and should not be construed as financial product advice, investment advice, or a recommendation to buy, sell, or hold any financial product or security. Lumix Traders Pty Ltd is not licensed to provide financial product advice. We do not hold an Australian Financial Services Licence (AFSL) under the Corporations Act 2001 (Cth). Nothing contained in this material constitutes financial advice, and it should not be relied upon as such. Readers are strongly urged to consult with a licensed and qualified financial adviser before making any investment or financial decision.

The views and opinions expressed in this material are current as of the date of publication and are subject to change without notice. Lumix Traders Pty Ltd has no obligation to update or revise any information following publication. Economic and market commentary presented herein reflects a series of assumptions and judgments as of the date of publication. Actual outcomes will vary. Forecasts and analysis are subject to significant uncertainty and should be viewed as one of a broad range of possible outcomes, not as predictive statements of fact.

Past performance is not indicative of future results. The value of financial assets can go down as well as up. Capital is at risk. This material is not intended for distribution to, or use by, any person in any jurisdiction where such distribution or use would be contrary to applicable law or regulation.